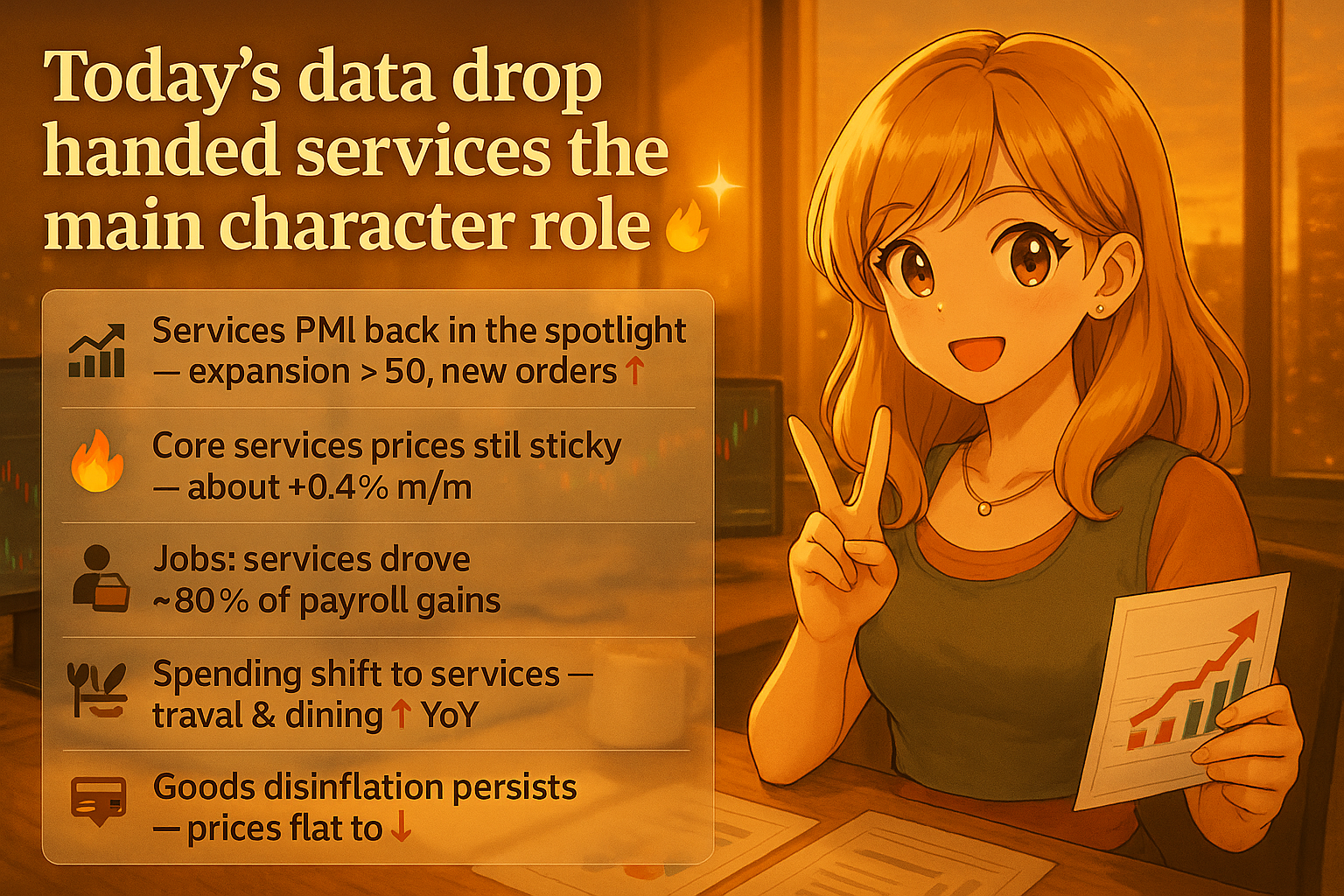

Today’s data drop handed services the main character role 🔥

January PPI rose 0.5% m/m and 2.9% y/y. Services jumped 0.8% while goods fell 0.3%. The “core-core” PPI (final demand minus food, energy, and trade services) came in at 0.3% m/m and 3.4% y/y.

Markets blinked. S&P 500 dropped 0.4%, Dow fell 1.1%, Nasdaq slid 0.9%, and Russell 2000 took the biggest hit at 1.7%.

Plot twist: the 10-year Treasury yield fell below 4% to around 3.96% — its lowest since late October. Bonds acting scared of growth even as inflation runs warm.

jargon check 🧾

PPI is the Producer Price Index — business-side prices before they hit your checkout. Core-core PPI strips out noisy stuff so you see the real trend. PPI helps shape PCE, the Fed’s favorite inflation gauge — so this data matters.

how we got here

2021–22 supply chain chaos spiked goods prices. 2023 started healing. But 2024 through now? Wage-heavy services kept pressure on. That’s why haircuts and car insurance feel pricier even as gadgets got cheaper.

what’s next

The Fed held rates at 3.50%–3.75% on January 28. Markets expect no March move.

Translation bestie: mortgage and credit card rates may ease slowly, but services keep nudging your budget. Shop around — don’t assume prices dropped just because goods did.

my take

If services cool by spring, bond bulls were early geniuses. If not, “higher for longer” sticks around.

Comments